Waiting for the perfect home or the perfect time? Here’s what the wait is really costing you

Posted on

Waiting for the “right time” to buy? It might be costing more than you think.

Every month spent sitting on the sidelines adds up – rent paid, property prices rising, and equity that never gets the chance to grow. For many Canberrans holding out for the perfect moment (or the perfect home), the real story is in the numbers.

Take Sarah and James. Both 40, with a four-year-old daughter and they’re renting in Canberra for $750 a week. They’ve built solid careers and have around $40,000 in savings – but like so many, they’re stuck in the “almost ready” phase. The deposit doesn’t quite feel big enough. The dream home hasn’t appeared. Maybe next year.

But here’s the thing: waiting comes at a cost – and the options available right now might be more within reach than they realise.

First, what is that rent adding up to?

$750 a week feels manageable. Until you add it up.

Every dollar of that is gone. No equity, no asset. It is the landlord’s return, not theirs.

An opportunity worth considering now

Sarah and James have $40,000 saved, which is exactly five per cent of an $800,000 property. Under the federal government’s Home Guarantee Scheme, eligible buyers can purchase with just a five per cent deposit, with the government guaranteeing the gap, and no lenders’ mortgage insurance to pay. For couples earning up to $200,000 combined, with an eye on a property under the ACT price cap of $900,000, the five per cent deposit scheme may be worth exploring with a qualified mortgage broker or financial adviser.

Stamp duty is an additional upfront cost to factor in, though the ACT’s Home Buyer Concession Scheme may reduce or eliminate this depending on income. This is worth talking to a mortgage broker about.

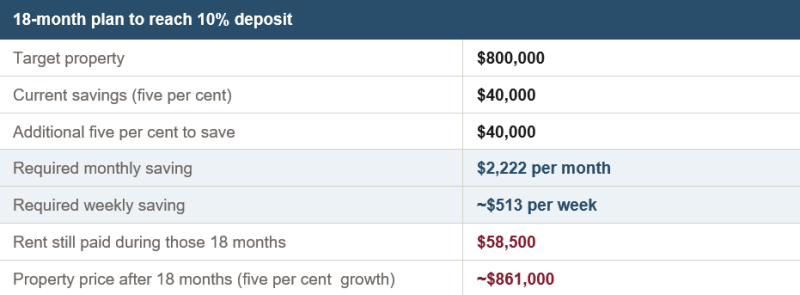

The 18-month savings plan

If Sarah and James choose to knuckle down and save the extra five per cent first, to reach a 10 per cent deposit and reduce their borrowing, here is what that plan looks like.

Saving $2,222 a month is a serious commitment. It means real trade-offs: less travel, fewer dinners out, buying second hand and being intentional about every dollar that leaves your account. Remember, it’s not forever. It’s choosing future security over present comfort. It also has to be considered with respect to the $58,500 in rent paid during those 18 months that builds zero equity, and a property that is now $61,000 more expensive than it is today.

Waiting an extra 18 months costs around $190,500 in rent paid, a bigger deposit, and higher repayments over the life of the loan.

Worth noting: a five per cent deposit does mean more debt. And with the RBA having raised the cash rate twice already in 2026, with more rises possible, that difference matters. The monthly repayment on a 95 per cent loan is around $760 more than on an 80 per cent loan if interest rates are six per cent. But that gap narrows quickly once you factor in what renting while you save is actually costing.

The perfect property problem

For many couples like Sarah and James, the delay is not often just about the deposit. It is about holding out for the right home, in the right location, with the right specs. More light, modern finishes, a tidy garden. These things matter, but they carry a cost that compounds with every month of waiting. Historically, some buyers have found that a well-selected property purchased at the right time has outperformed waiting for a perfect one.

Balancing realistic expectations with market timing is an important consideration in any property decision.

Plus, once you’re in, you can make it your own over time; new carpet, a kitchen refresh, a coat of paint. And if you’ve already built the habit of saving regularly, you’re in a great position to fund those upgrades when the time is right. Better still, the equity you build as a homeowner can work for you down the track, helping to fund those improvements. It’s a financial tool that renting simply doesn’t offer.

There is also something the numbers cannot fully capture. Rental properties change hands, leases end, and families are forced to move. For Sarah and James, whose daughter is approaching school age, every move risks disrupting friendships, changing schools, and unsettling a child who has just found her footing. Owning means staying put on their own terms.

The bottom line

Waiting feels cautious. It feels responsible. Because you want certainty before making one of the biggest financial decisions of your life. The problem is that certainty rarely comes, and the Canberra market rarely waits with you.

Of course, buying isn’t the right goal for everyone and that’s completely valid. Renting offers flexibility, and for many people at different stages of life, it’s absolutely the right choice.

But if homeownership is on your radar? The short-term trade-offs: a tighter budget, a home that is not quite perfect yet, are small against what decades of ownership can deliver. Owning a home is one of the most powerful foundations a family can build, not just for the equity it creates, but for the stability, the security, and the certainty of knowing that where you live is yours.

Modelling assumptions and disclaimer

Evans and Partners, May 2026. Target property $800,000; five per cent deposit $40,000; HGS loan $760,000 at 6.5 per cent p.a. over 30 years; monthly repayment $4,804; five per centp.a. property growth (Canberra long-run conservative estimate); current weekly rent $750. Total cost of delay includes rent paid during delay, additional deposit required at the higher price, and higher loan repayments over the 30-year loan life. Home Guarantee Scheme eligibility is subject to income caps, property price caps, and Housing Australia criteria. Figures are illustrative only and do not constitute personal financial advice.

Sources: ABS Total Value of Dwellings December Quarter 2024; RBA Cash Rate April 2025; Domain ACT Rental Report Q1 2025; Housing Australia Home Guarantee Scheme eligibility criteria 2024-25.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.