The Pay Gap is smaller in Canberra. The Super Gap isn’t.

Posted on

Canberra women are the highest paid in the country. So why are they still retiring with less?

Canberra has structural advantages that most Australian cities don’t: a workforce dominated by the Commonwealth Public Service, higher-than-average incomes, and one of the lowest gender pay gaps in the country. On paper, ACT women should be better placed for retirement than almost anyone else.

The data tells a more complicated story.

The Canberra advantage

The Commonwealth Public Service drives genuine pay equity advantages that flow directly into super. According to the ABS, the ACT gender pay gap on full-time ordinary time earnings is just 5.3 per cent, less than half the national average of 11.5 per cent. And because super is paid as a percentage of salary, a smaller pay gap means smaller contribution gaps and a smaller shortfall at retirement.

Public sector employer contribution rates of 15.4 per cent also compound this advantage from day one. That’s $3,400 more per year into super on a $100,000 salary compared to the national minimum of 12 per cent, before returns are even factored in.

It’s worth noting, though, that the ACT’s private sector gender pay gap remains closer to the national average of 21.1 per cent. Canberra isn’t uniformly equal; the advantage is concentrated in the public sector, and not every Canberra woman works there.

Why the retirement gap persists anyway

Nationally, ATO data shows women aged 60 to 64 hold a median super balance of $163,218, compared to $219,773 for men, a 25 per cent gap at exactly the point most people are preparing to stop work. Canberra’s higher income base helps locally, but the structural forces that erode women’s super during their working years are present here too.

Career breaks for caring, part-time work, and the persistent leadership gap all take a toll. WGEA data shows women who reach CEO level still earn $83,493 less in base salary than their male counterparts which widens to $185,335 when super, bonuses and overtime are included. Even in Canberra, where the overall gap is smaller, women are less likely to hold the highest-earning roles.

Timing compounds the problem further. Women who retired in 2024–25 did so at an average age of 62.7, compared to 64.9 for men, which is more than two years less of contributions and compounding, followed by a longer retirement to fund. A smaller balance stretched over more years leaves little room for the unexpected.

The consequences show up starkly in the retirement income data. Nationally, 30 per cent of retired women rely on a partner’s income to meet their living costs, compared to just 9 per cent of retired men. And here’s the Canberra figure that cuts through: despite being the highest-paid women in the country, ACT women make up 60 per cent of all ACT age pension recipients. It’s the highest female share of any state or territory in Australia, and well above the national average of 55.6 per cent.

It shows that higher earnings alone don’t insulate women from pension dependency in retirement.

Financial independence is not a given; it’s built.

What you can do about it

The structural advantages of working in Canberra are real but they don’t work automatically. Here are three practical ways to make them work harder for you:

Be smarter with what you already earn

For many Canberra women in the Commonwealth Public Service, pay increases aren’t negotiated individually, they’re built into enterprise agreements, delivered incrementally and predictably. That regularity is an advantage most private sector workers don’t have. The question is whether those increases are working as hard as they could be.

One of the most effective ways to put an enterprise agreement pay rise to work is to redirect a portion into super before it hits your bank account. And, if there’s one thing super loves, it’s time. Even small contributions made consistently can grow significantly over the long term.

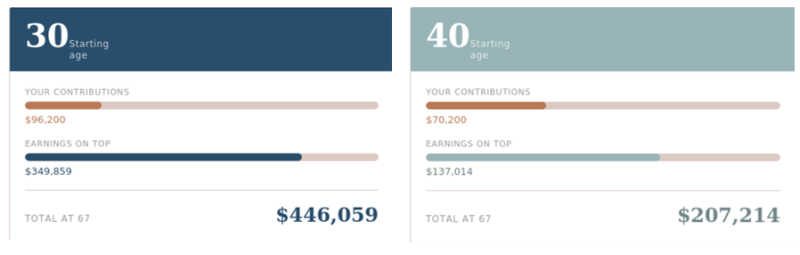

Consider the cost of a night out in Braddon. Let’s say its $100 – which is perhaps conservative these days if you add in a few cocktails and an Uber home. Redirecting that spend into super on a fortnightly basis, at average balanced super fund returns of 7 per cent, could look something like this:

Projections are for illustrative purposes only and based on assumed rates of return which are not guaranteed. Modelling by Evans and Partners.

The ten-year delay and spending that $100 per fortnight instead of investing it, costs nearly $239,000 in lost growth. Same $100. Just used wisely. That’s the power of compounding.

For public servants, most departments make voluntary contributions straightforward through salary sacrifice. But, if you’re a contractor or business owner, a personal contribution when cashflow allows could achieve the same result. The maths works in your favour twice: you pay less tax now, and your super compounds for longer.

The key is consistency, not perfection.

Review your investment strategy

Women are more likely than men to select conservative investment options within super. If you’ve never changed the default option your employer first put you in, it’s worth checking whether it suits where you are now. Particularly if you’re more than 10 years from retirement, considering growth-focused investment options may deliver meaningfully better long-term outcomes.

For instance, a one per cent annual improvement in returns, sustained over 30 years, could produce a retirement balance approximately $339,000 higher. For many women, that’s the difference between the age pension and financial independence.

Don’t let the default setting make this decision for you.

Plan ahead for career breaks

Career breaks, whether that’s for parental leave, caring responsibilities, or a shift to part-time work, are among the single biggest contributors to the super gap. A little planning before the break can significantly reduce the impact: voluntary contributions while you’re working full-time, carry-forward concessional contribution rules to top up in higher-earning years, and reviewing your investment settings as your circumstances change.

From 1 July 2025, the government began paying superannuation on Commonwealth Paid Parental Leave, a reform that directly benefits ACT women taking government-funded leave. It’s a meaningful change, but it doesn’t replace the need to actively manage your super around career transitions.

Your super doesn’t have to stop growing just because your circumstances change.

The advantage is yours to use

Canberra women have structural advantages that most Australian women don’t. But the retirement data shows those advantages don’t translate automatically into better outcomes. The 15,745 ACT women currently on the age pension are a reminder that higher earnings during your working life are only part of the picture.

Staying across your balance, your investment strategy, and your contribution settings, particularly around career breaks, is what converts a structural advantage into actual financial independence.

Think of it less as admin and more as future-you maintenance.

Sources and disclaimer

- ATO, Taxation Statistics 2021–22 (published 2024). Median superannuation balances by age and gender.

- WGEA, Australia’s Gender Equality Scorecard 2024–25 (published March 2025). Public sector and private sector gender pay gaps; CEO remuneration gender pay gap.

- Super Members Council (SMC), Economic Security in Retirement: How Life Events Affect Older Australian Women, 2025.

- ABS, Retirement and Retirement Intentions, Australia, 2024–25.

- ABS, Average Weekly Earnings, Australia, November 2025. ACT and national full-time adult AWOTE by sex.

- DSS, Benefit and Payment Recipient Demographics – Quarterly Data, December 2025. Age pension recipients by state and gender.

This article was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (‘Evans and Partners’), a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457). The information is general in nature and prepared without considering your objectives, financial situation or needs. You should seek professional advice before acting. Past performance is not a reliable indicator of future performance. Neither E&P Financial Group nor its related entities make any representation as to the accuracy or likelihood of fulfilment of any forward-looking statements. Evans and Partners Financial Services Guide, which sets out our services, remuneration and potential conflicts, is available at www.eandp.com.au.