Is the investment property dream still worth it?

Posted on

For years, owning an investment property has been Australia’s favourite dinner party flex. But the 2026 federal budget quietly shifted the rules and in Canberra especially, the maths looks different now.

You know the one. The colleague at work drinks who steers every conversation back to their rental in Gungahlin. The friend who casually mentions their “portfolio” at a Braddon brunch. The neighbour who nods knowingly every time interest rates come up, because they’ve “done the numbers.”

Investment property has been Australia’s unofficial national hobby for decades. And in Canberra – with its stable incomes, strong public sector wages and a property market that has historically rewarded patience – it’s been particularly popular.

Unless you’ve been living under a rock, you’ve heard about the budget. And if you’ve been half-paying attention, the words “negative gearing” have either made you want to get on board or jump ship entirely.

So, what actually changed?

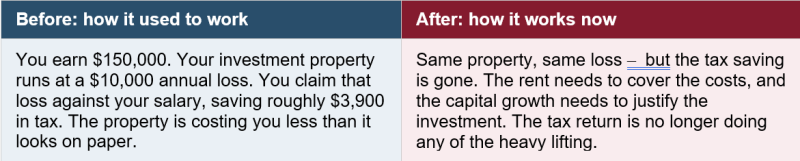

The headline measure is a restriction on negative gearing. In plain terms, negative gearing is what happens when your investment property costs more to hold than it earns in rent, and until now, you could use that loss to reduce your other taxable income, including your salary. For anyone on a decent Canberra wage, that tax saving has been a meaningful part of making the numbers stack up.

From 1 July 2027, that offset disappears for established properties purchased after budget night (12 May 2026). Losses can still be carried forward and used against future rental income, but you can no longer use them to reduce your wage income in the way people have been doing for years.

The tax benefit that made negatively geared property attractive to higher earners (offsetting rental losses against a good salary) is the exact benefit that’s being removed.

Why Canberra feels this more than most

This is where it gets locally relevant. The Canberra investor who has been quietly smug about their tax deductions is typically someone on a solid income – a public servant, a contractor, or a dual-income household doing well. That’s precisely the profile the budget change is designed to affect most.

The higher your income, the more valuable that wage-offset deduction was. Losing it doesn’t make investment property worthless, but it does make the cash-flow equation tighter, and now, the rental return and capital gain potential really need to stack up on their own.

*For illustrative purposes only. This is not a projection of individual outcomes.

You can’t rely on the tax benefit to make property investing a good strategy anymore

What still works

It’s worth being clear: investment property hasn’t stopped making sense. It just requires more honest maths. A few things worth knowing:

- Already own an investment property? Nothing changes. Properties held before budget night are fully protected under the existing rules for as long as you keep them.

- New builds are exempt entirely. If you’re considering an investment property and open to something newly constructed, full negative gearing is retained and in some cases the tax treatment is now more favourable for new builds than established properties, which is exactly what the government intended.

- Rental yield matters more now. A property with a strong rental return one that is close to positively geared is far less exposed to this change than one that was always relying on the tax offset to stay viable.

The bottom line

If investing was on your radar, it might be worth broadening the conversation beyond property. While an investment property can still make sense, if the main appeal was the EOFY tax return, the numbers look quite different now.

The good news is there are other ways to grow wealth that have never relied on that tax offset to begin with: diversified shares, managed funds, and superannuation among them. They don’t come with an unreliable tenant, liquidity problems, or the ongoing costs that quietly eat into your returns. For some people, that simplicity is genuinely underrated.

It’s also worth noting that none of this is law yet, the changes still need to pass the Senate and the detail may shift. So, if the budget has prompted a mild panic about your property plans, take a breath. A rushed decision made on a proposed change is rarely the right one.

If you are planning ahead and not sure which path is right for you, that’s exactly the conversation worth having with an expert before you commit to anything.

Assumptions and disclaimer

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.